Would you want to know how 401k loans work? You borrow from your retirement assets rather than from a lender when you take out a 401(k) loan.

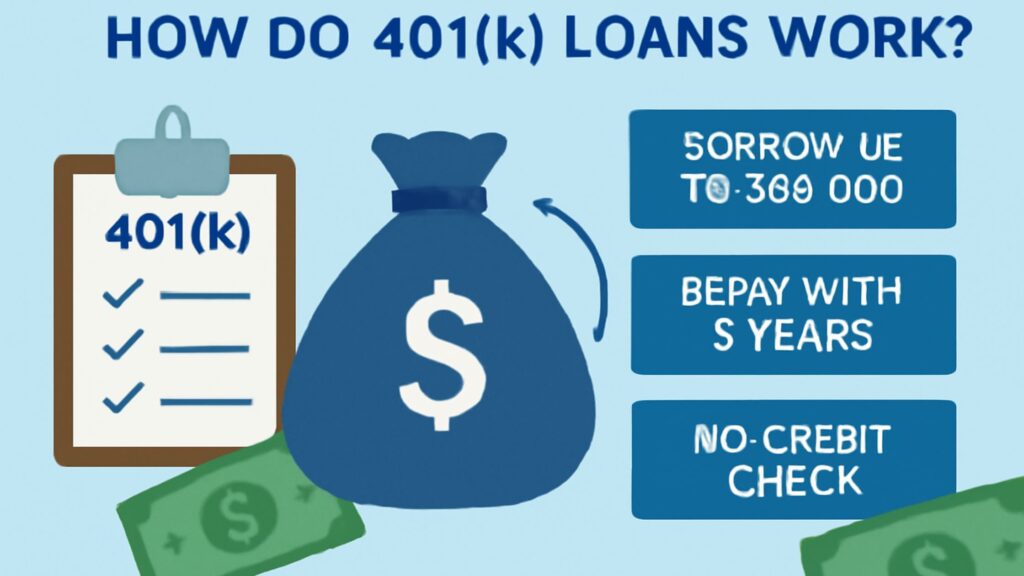

As a result, 401(k) loans are often more straightforward for people with weak credit, as no credit check is required to qualify, and the interest rates are typically low.

However, not all plans allow you to borrow against your retirement assets. You should know several 401(k) loan requirements if you do.

1. Withdrawal Restrictions:

You can borrow up to $50,000 from your 401(k) or half of your vested amount, whichever is smaller. Some plans may require a minimum withdrawal amount.

Your maximum withdrawal amount will be lowered if you have an outstanding loan from the program during the one year before your new loan.

2. Loan Term Limits:

The maximum loan period is five years. However, you may be able to pick a shorter term if it matches your needs. Borrowers looking to fund a housing down payment are exempt, though.

3. Potential Spousal Permission Requirement:

Some plans require married people to produce written proof of spousal consent to take out a 401(k) loan.

4. Tax Implications:

Repayments are usually taken directly from your salary after taxes, and you’ll have to pay taxes again when you withdraw the money when you retire.

5. Inherent Risks:

If your job is terminated before you’ve paid off the loan, you’ll most likely be obliged to repay the amount within 90 days.

Otherwise, you would have to pay income taxes on the amount borrowed. If you are under 5912, you may be liable to an extra 10% early withdrawal penalty.

ALSO READ – Length Of 401k Loan

Now, let’s get started.

What Exactly Is A 401(K) Loan?

A 401(k) loan allows you to borrow money from your retirement account to repay yourself.

Even if you are lending money to yourself, it is still considered a loan if you charge interest for the amount you are responsible for.

When you borrow from your 401(k), you’ll get the same terms as any other loan: A repayment schedule depends on the amount borrowed and the interest rate locked in.

According to IRS regulations, you have five years to return the loan unless the funds were used to purchase your primary residence, in which case you have extra time to repay.

However, there are several significant drawbacks to a 401(k) loan. While you will pay yourself back, one key disadvantage is that you still withdraw money from your tax-free retirement account.

And the less money you have in your plan, the less money you will have over time. Even if you pay it back, it will take less time to mature.

Furthermore, if you have a standard 401(k), you will be repaying the pre-tax monies in the account with your after-tax earnings; thus, repaying the loan will take even longer working hours.

The Benefits And Drawbacks Of A 401(K) Loan

Benefits

There Is No Loan Application.

You don’t have to apply for a loan to borrow against your 401(k), and you may not have to explain why you need the money because you’re making your own money out of your account.

You must still supply some information to your plan’s administrator, but the procedure is not as complicated as qualifying for a bank or credit union loan.

Credit Reports and Credit Scores

Similarly, because you’re using your own money, your credit score—a statistic used to assess your creditworthiness to future lenders—has no bearing on your ability to withdraw the funds.

Furthermore, borrowing cash does not result in a hard inquiry (when a lender wants to look at your credit record). Thus, your credit score will not suffer as a result.

Because your plan administrator does not record your repayments to the three major credit reporting agencies—Equifax, Experian, and TransUnion—if you do not return the entire amount, your credit score and reports will not be harmed.

Interest Rate Reduction

You should be able to borrow at a cheaper interest rate than you would at a bank. The prime rate + 1% or 2% is the standard interest rate you must pay.

The prime rate—the interest rate that banks charge their least-risky business clients—was 3.25 percent in January 2022.

There Are No Outstanding Taxes.

The Internal Revenue Service does not require you to pay income tax or a 10% early withdrawal penalty on the money you remove as long as you pay it back on time; this is usually within five years but can be as long as 15 years if you took the money out to buy a property.

There is usually no penalty for returning the money to your 401(k) before the loan period ends.

Automatic Withdrawals

You refund the money through deductions from your salary. The process should be simple if you stay with the same employer over the payback period.

Drawbacks

Loans May Not Be Granted.

Because some firms do not allow employees to borrow from their retirement funds, a 401(k) loan may not be an option for you.

Contact your plan administrator or visit its website to determine if loans are permissible.

You are not permitted to borrow from a plan established by a former employer. You may, however, roll over the balance of that plan into your current employer’s plan and then borrow the money.

Borrowing Restrictions

You can borrow up to $50,000 from your 401(k), or 50% of the sum, whichever is smaller.

1 If your plan permits you to take out several loans, you may not borrow more than that amount or percentage.

Potential Gains Are Lost

Because the money you withdrew is no longer in a mutual fund or another investment, you may miss out on profits that your nest egg would have made otherwise.

This wasted opportunity to generate additional money from that money is referred to as an opportunity cost.

Attachment Of The Employer

Suppose you quit your job before repaying your loan. In that case, any remaining balance may be considered a taxable distribution to you until you return it in full within a specific time frame.

Trying to prevent that circumstance may keep you in a job longer than you would like.

Giving Up Bankruptcy Relief

Your 401(k) assets are protected from creditors during bankruptcy proceedings.

If you borrow funds from the plan to help pay bills but then become insolvent and file for bankruptcy, creditors may seize any remaining withdrawn funds.

ALSO READ – How Can I Retire In 7 Years?

How To Apply For 401(K) Loans

Depending on your plan sponsor, the procedure for receiving a 401(k) loan will differ.

However, because no credit check is usually necessary, you can inquire about the rates and costs of a 401(k) loan without jeopardizing your credit score. Here’s how to start the procedure.

1. Review Your Strategy Documentation.

401(k) loans are not accessible in all plans, so check your plan document to ensure they are available via your provider.

You may be able to access these through an online account, or you may have to request them by mail or from your human resources department. Look for further information such as:

Minimum and maximum monetary values

Maximum number of loans outstanding

Terms of repayment

APR

2. Determine How Much Money You Need To Borrow.

Check that this amount is within the IRS and your provider’s restrictions.

3. Create A Payment Budget For Yourself.

Total your monthly costs. Can you make timely payments while covering vital expenditures such as rent and utilities?

If not, you may need to borrow from another source or acquire more significant income over an extended period.

4. Fill Out The Loan Application.

If you’re ready, go through the application process outlined by your provider.

You may be allowed to finish the application online, or you may be required to fill out papers with your human resources department.

5. Obtain Approval.

If your request is accepted, you should have access to your funds within a few days.

If you’re unsure if a 401(k) loan is good for you, there’s nothing to lose by seeking further information from your provider.

To make the best decision, compare personal and secured loan rates, such as a home equity loan. Before applying for a loan, just be sure you can keep up with the payments.

How Long Does It Take To Receive A 401(K) Loan?

After the approval procedure is finished, you will get all loan-related information.

It might take a few days to a week or two, depending on your plan’s administrator and how you receive your payments.

Most plans will make payment within two to three business days of loan approval.

A physical check is one method of receiving your payments. If you choose this option, the assessment may take an extra day from your plan administrator’s facility to the post office.

The cheque will be delivered to your home after the standard postal delivery time.

When it arrives, it must be deposited into your account, which may take a day or two, depending on your bank.

Your plan administrator can directly deposit the monies into your bank account, which is a much faster alternative.

Once the loan is granted, the transfer will take a few days to complete. The money will then appear in your account within a day or two.

ALSO READ – How Can I Improve My Financial Skills

What Is The Interest Rate On A 401(K) Loan?

The beautiful thing about 401(k) loans is that the interest is repaid into your account.

Unlike a traditional loan, when interest is paid to the bank, the interest paid on a 401(k) loan is paid to the future you.

Another advantage is that the interest rate “charged” on a 401(k) is often higher than the market rate of return.

Sure, it’s your money being repaid at a higher rate, but by the time the loan is paid off, you’ll have replenished your 401(k) to even greater levels.

Furthermore, when you replenish your 401(k) balance with each contribution, that amount will grow as the assets rise.

What Are The Requirements For A 401(K) Loan?

The IRS determines the duration of 401(k) loans. Borrowers of 401(k) loans must typically return the loan within five years to avoid taxes and penalties.

If you take out a 401(k) loan to support the down payment on a property, the IRS will extend the payback period to 15 years.

This assists in breaking down the payments into smaller quantities. Although the opportunity cost of deferring the complete repayment is the missed development opportunity for your 401(k),

Furthermore, because of the COVID-19 epidemic, current legislation has increased the typical payback period from five to six years, providing borrowers an extra year to repay their debts.

Another feature of this law is that loan amount limitations have been raised to $100,000 or 100% of the vested balance.

ALSO READ – How Can I Invest With No Money

What Happens If You Fail To Repay A 401(K) Loan?

Any debt default is never a brilliant idea. If you are late on regular loans, your credit will suffer, and the loan sum will be sent to collectors.

If you do not return your 401(k) loan, you may be in danger. Your credit will not be affected, but the IRS will consider the defaulted loan an early retirement payout.

The loan balance will be deemed income and taxed at the income tax bracket determined by the loan and your yearly income. In addition, the IRS will levy a 10% penalty tax on the remaining sum.

If you do not pay this by the IRS’s deadline, you will be liable to backed tax penalties and interest.

As a result, it’s critical to figure out how you will return the debt as soon as feasible.

What Motivates People To Take Out 401(K) Loans?

Participants can generally draw from their 401(k) for any reason as long as the plan permits.

Some plans may only allow loans for specified reasons, so verify the terms of your project before attempting to borrow.

Because you’re borrowing your own money and there’s no credit check, you may find getting accepted for a 401(k) loan simpler as long as you match the plan’s borrowing limitations.

In some situations, seeking consent from your spouse (if you’re married) may be required because your spouse may be entitled to half of your retirement assets if you divorce.

Here Are Some Examples Of 401(K) Loan Applications.

• Taking care of home expenditures and costs

• Saving for a down payment on a property

• Repaying high-interest loans

• Paying for medical expenditures

• Repaying taxes or owing money to the IRS

• Paying for required house repairs

• Covering educational fees

However, this does not mean that 401(k) loans are always a smart option. In truth, borrowing from retirement assets carries some significant hazards.

ALSO READ – Hedge Funds vs Retail Investors

The Best Reasons To Borrow From Your 401(K) (K)

The following are the top four reasons to go to your 401(k) for significant short-term liquidity needs:

1. Convenience And Speed

Requesting a loan in most 401(k) plans is quick and uncomplicated, with no lengthy paperwork or credit checks. Usually, it does not result in a credit inquiry or influence your credit score.

Many 401(k)s allow loan requests to be made with a few mouse clicks on a website, and cash may be in your hands in a matter of days, with complete secrecy.

A debit card, which allows several loans in tiny amounts to be done rapidly, is one innovation that some plans already use. 3

2. Repayment Versatility

Although laws require a five-year amortizing repayment schedule, you can repay most 401(k) loans sooner with no prepayment penalty.

Most plans allow debt repayment to be made simply through payroll deductions—but only with after-tax monies, not the pre-taxes that finance your procedure.

Like a conventional bank loan statement, your plan statements display credits to your loan account and your remaining principal balance.

3. Financial Advantage

Using your 401(k) funds for short-term liquidity requirements is unnecessary (other than a tiny loan origination or administration charge). This is how it usually goes:

You designate which investment account(s) to borrow money from, and those investments are liquidated for the loan period.

As a result, you forfeit any positive gains generated by such assets for a limited time.

And when the market is down, you may sell these investments at a lower price than before.

The advantage is that you avoid any additional investing losses with this money.

The cost advantage of a 401(k) loan is the interest rate charged on a comparable consumer loan, less any missed investment gains on the borrowed principal.

A plan loan might appeal when the cost advantage is expected to be favorable.

Remember that this estimate disregards any tax impact, which might boost the plan loan’s benefit because consumer loan interest is paid using after-tax earnings.

4. The Value Of Retirement Savings

Your 401(k) account loan repayments are typically reinvested in your portfolio’s investments.

You will reimburse the account somewhat more than you borrowed, and the difference is known as “interest.”

Suppose any missed investment profits equal the “interest” paid in. In that case, the loan has no (or a negative) influence on your retirement—that is, earnings potential is countered dollar for dollar by interest payments.

A 401(k) loan might enhance retirement savings if the interest paid exceeds any lost investment gains. However, remember that this will lower your personal (non-retirement) savings.

What Are Some 401(K) Loan Alternatives?

Borrowing from your 401(k) plan and paying yourself interest may seem like a brilliant idea when money is tight. But, before you borrow, consider all of your choices. Here are a few examples.

1. Think About A Home Equity Loan.

If you have equity in your house, you may be able to use it to qualify for a loan with a home equity loan.

Because the interest on a home equity loan may be tax-deductible, this may be a suitable alternative if you need the loan cash for house repairs and renovations.

2. Think About A Taxed Withdrawal.

If you require cash due to financial difficulty, consider a hardship withdrawal rather than a loan (what is considered a hardship withdrawal varies by plan).

You’ll almost certainly have to pay income taxes on the distribution, but you could be eligible for an exemption to avoid a 10% early withdrawal penalty.

There are certain drawbacks to hardship withdrawals, so do your homework carefully.

If your distribution is due to financial difficulty caused by the coronavirus, you may also be entitled to have the 10% penalty lifted.

3. Consider Obtaining A Personal Loan.

If you have strong credit, you may be able to get a personal loan with advantageous conditions. A personal loan may be used to pay for just about anything.

Furthermore, because they are often unsecured, you do not need to put up collateral to secure the loan.

ALSO READ – For Mortgage Loans: What Is Prepayment Risk

Final Thoughts

Depending on your financial condition, a 401(k) loan might be an excellent way to get money to pay off high-interest debt or cover a hefty bill.

However, this loan may cost you money in certain situations, so it may not be the best option.

Remember that it is not the only choice; you should always consider all options before settling on a loan type.

If borrowing from your 401(k) is your only way to get the money you need, ensure you understand all the terms. It’s also critical to have a plan to repay the loan.

Finally, search for ways to pay off your 401(k) debt ahead of schedule by making extra payments, such as if you earn a windfall or a rise.

The sooner you pay off the loan, the sooner you may return to making returns on your investment, and the less likely you are to default on the loan or face a significant tax burden if you leave your employment.